Deal: 23andMe to go public via SPAC sponsored by the Virgin Group

Deal: 23andMe to go public via SPAC sponsored by the Virgin Group

Genetic testing for consumers and biobank data for drug development

The “Deal” series of articles discuss business agreements and the implications. These articles offer unique and integrated perspectives to the significance of the agreements.

Highlights and takeaways

23andMe is a leader in direct-to-consumer (DTC) genetic testing and offers insights into ancestry, carrier status, disease risks, pharmacogenomics, and more. Its technology platform involves genotyping with single nucleotide polymorphism (SNP) microarrays and phenotyping with online surveys.

Through these consumer services, 23andMe has built up a massive biobank. The accumulation of SNP-based genotypes paired with survey-based phenotypes gives 23andMe the ability to develop precision medicine assets and form robust collaborations with pharmaceutical companies.

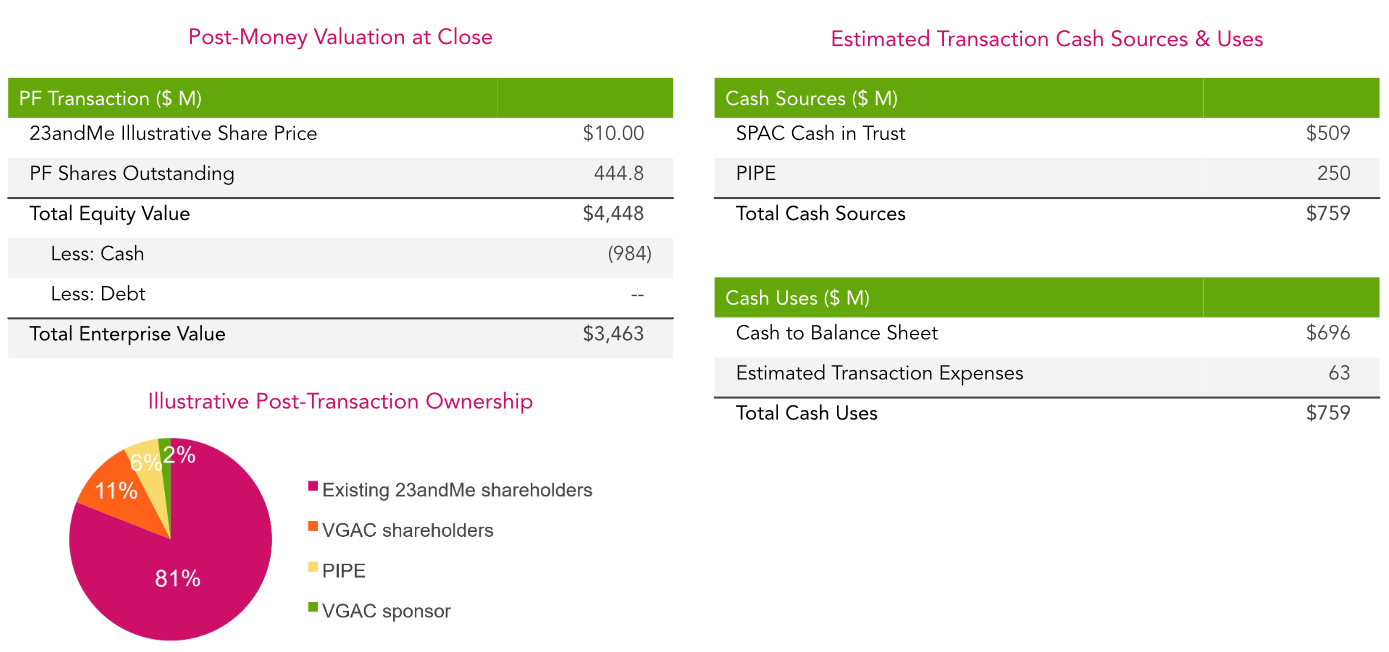

23andMe will be going public through merger with the Virgin Group’s SPAC with an implied enterprise value of $3.5B. This transaction will bolster its cash position by $759M ($509M from cash in trust and $250 from PIPE financing) and enable 23andMe to accelerate customer acquisition and drug discovery efforts. Also, this financing will help advance their wholly-owned checkpoint inhibitor toward first-in-human clinical trials.

Direct-to-consumer genetic testing

23andMe was founded in 2006 and its name refers to the 23 pairs of chromosomes, in which a normal human has 22 pairs of autosomes and 1 pair of sex chromosomes. 23andMe offers direct-to-consumer (DTC) genetic testing based on genotyping single nucleotide polymorphisms (SNPs) from saliva samples. Due to the overwhelming conservation of the human genome, SNP genotyping offers an affordable yet robust alternative to, for example, whole genome sequencing. Briefly, SNPs are simply single nucleotide substitutions that could reside within a coding or non-coding region of the genome. If the SNP falls within a coding region, it may change the amino acid sequence of the expressed gene. However, due to codon degeneracy, the SNP in a coding region could be a silent mutation and therefore not change phenotype. If the SNP falls within a non-coding region, gene expression could be affected due to altering mechanisms like transcription factor recognition, mRNA degradation, etc. Of course, the SNP in a non-coding region may not have an observable effect. SNP genotyping was initially applied as a forensics tool (ref), but has since been widely used for ancestry reconstruction (ref) and predicting disease predispositions (ref).

Source: 23andMe website

23andMe had tumultuous beginnings, particularly due to nascent regulatory policies around DTC genetic testing in the United States (ref). In 2008, the “retail DNA test” from 23andMe was considered the best invention of the year by Time Magazine (ref). That same year, President George W. Bush signed into law the Genetic Information Nondiscrimination Act (GINA), which prohibited genetic discimination for health insurance and employment (ref). Over the next years, 23andMe had extensive discussions with the FDA regarding the regulation of its genetic testing services. In 2013, the FDA ordered the company to discontinue marketing its personal genome service (PGS) as an unauthorized device due to its description as “the first step in prevention” (ref). Resultantly, 23andMe was only able to provide ancestry information and raw genetic data without interpretation (ref). In 2015, the FDA authorized the PGS for Bloom Syndrome Carrier status as the first DTC genetic testing (ref). Since then, 23andMe has received additional regulatory approvals for its DTC services. Most notable is the authorization of the PGS Genetic Health Risk (GHR) for ten diseases or conditions: Parkinson’s disease, late-onset Alzheimer’s disease, Celiac disease, Alpha-1 antitrypsin deficiency, early-onset primary dystonia, factor XI deficiency, Gaucher disease type 1, glucose-6-phosphate dehydrogenase deficiency, hereditary hemochromatosis, and hereditary thrombophilia (ref). In contrast to the previously approved tests for whether an individual was a hereditary carrier, these PGS GHR tests would provide genetic risk assessments (yet without serving as clinical diagnoses).

Source: 23andMe corporate presentation

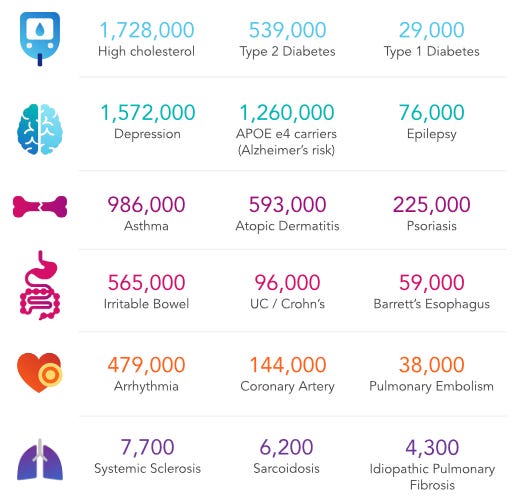

In addition to providing carrier status and disease risks, 23andMe also offers pharmacogenomics testing results that probe drug sensitivity phenotypes like adverse drug reaction (ADR), efficacy, and dosage adjustment (ref). One report also includes information on acetaldehyde toxicity, which is related to the recreational use of alcohol. Recently, 23andMe was able to identify strong associations between blood type and COVID-19 susceptibility (ref). Interestingly, the study found that blood type O is a risk factor for seasonal flu, yet is protective against severe COVID-19. However, the authors noted that phenotypes were derived from online surveys and that respondents may be biased toward a healthier case population. Generally, the phenotypes determined through 23andMe PGS are derived from online surveys that about 80% of customers complete.

Massive biobank enables unique opportunities in drug development

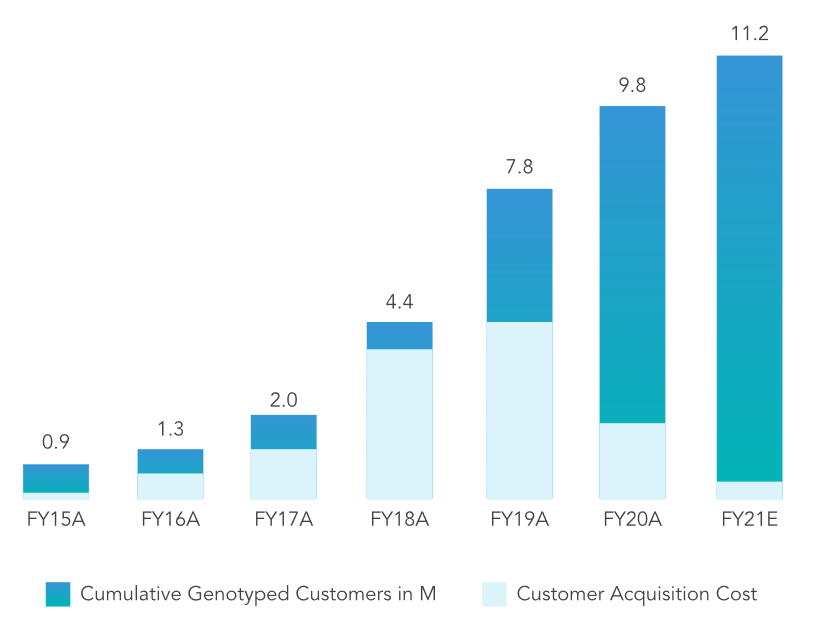

Given its capacity to conduct D2C genetic testing in an affordable and scalable manner, 23andMe can build an enormous biobank on populations that clinical trials wouldn’t normally be able to recruit (many healthy consumers vs. few healthy volunteers or sick patients). 23andMe genotyped its 1 millionth customer in 2015 (ref) and currently has over 12 million customers (ref). The company continues to amass genotype-phenotype data and is quickly approaching the (at least) 15 million customers that AncestryDNA has (ref).

23andMe has leveraged this database for research collaborations with academic and industry partners (ref). For example, 23andMe and Genentech conducted a genome-wide association study (GWAS) to identify risk loci for Parkinson’s Disease (PD) (ref). The analysis was performed on consenting customers of 23andMe: nearly 6.5k PD cases and over 302k control subjects. Interestingly, 2.3% of PD cases and 0.18% of control subjects were carriers of the G2019S mutation of leucine-rich repeat kinase 2 (LRRK2). In addition to reaffirming glucocerebrosidase (GBA) and transmembrane protein 175 (TMEM175) as known candidate genes associated with PD risk, several new candidate genes were identified. For example, genes involved with lysosomal dysregulation like cathepsin B (CTSB) or galactosylceramidase (GALC) were identified to contribute to PD risk. This was the largest meta-analysis for PD and nearly doubled the number of candidate genes to date.

Source: Chang et al. 2017

Following the publication of this study, 23andMe was able to establish numerous partnerships. In 2018, 23andMe secured a collaboration with GlaxoSmithKline ($GSK) for both advancing therapeutic programs and recruiting patients with defined LRRK2 mutations for PD clinical trials (ref). (On a related note, see this Insights article on Biogen’s recent deal with Denali for its LRRK2 program.) The two companies agreed to evenly co-fund the efforts, and that GSK would invest $300M into 23andMe. At the time of this agreement, 23andMe had 5 million customers. In 2019, 23andMe secured collaborations with digital health company Lark Health (ref) and RNAi therapeutics company Alnylam Pharmaceuticals ($ALNY) (ref). Evidently, 23andMe is aggressively expanding into patient care and drug discovery. The therapeutics division of 23andMe has listed several job openings, e.g. scientists in immuno-oncology or protein engineering, CMC process development leads, and clinical trial managers (ref).

Source: 23andMe corporate presentation

While most of its therapeutic programs (including the CD96 program in phase 1 clinical trials) are jointly pursued by GSK, 23andMe has a wholly-owned P006 program (ref). This asset appears to be an immune checkpoint inhibitor. Last year, 23andMe discovered and out-licensed the rights to a bispecific monoclonal antibody (bsMab) that blocks all three isoforms of IL-36 to Almirall, a pharmaceutical company focused on dermatology (ref). This pan-IL-36 inhibitor could be a therapy for autoimmune and inflammatory diseases, including psoriasis (ref), and is the first molecule to be developed using consumer data (ref).

Source: 23andMe corporate presentation

Thus, 23andMe has an impressive business model centered on its growing biobank. 23andMe can provide genetic testing services directly to consumers, as well as utilize these data to generate therapeutic assets and form partnerships with other pharmaceutical companies. Not only are these activities highly valuable, 23andMe greatly benefits from the network effect from multiple angles (ref). Moreover, the cost for acquiring customers is rapidly decreasing. Arguably, there are limitations to the reliability of SNP-based genotyping and survey-based phenotyping, as well as challenges to rapidly expand its consumer base. There are also considerable regulatory risks, demonstrated by its historical clashes with the FDA, and serious scrutiny regarding the ethics of its business (ref). This includes concerns about the significant investments by Google (now Alphabet) and how 23andMe will use its consumer data (ref, ref).

Transaction terms for going public

Private companies can go public by merging with an existing special purpose acquisition company (SPAC) (ref). Last week, 23andMe announced that it will merge with VG Acquisition Corp ($VGAC), a SPAC sponsored by the Virgin Group and incorporated last year (ref). Interestingly, the Virgin Group had invested in the series A financing (and onwards) of 23andMe (ref). The new company will have a cash position in excess of $900M and an implied enterprise value of $3.6B. The transaction will be funded by $509M cash in trust from VGAC and $250M from a committed private investment in public equity (PIPE) financing. 23andMe cofounder Anne Wojcicki and Virgin Group cofounder Richard Branson will be each investing $25M into the PIPE. Also participating in the private placement will be Fidelity, Altimeter Capital, Casdin Capital, and Foresite Capital. Details on the sponsor agreement and the PIPE financing are available in SEC filings (ref).

Source: 23andMe corporate presentation

When VGAC IPO’d, it registered 46M units priced at $460M, each of which consisted of one class A share and one-third of a redeemable warrant (ref). The underwriters were also granted a 45-day option to purchase an additional 7.2M units at the IPO price. Thus, a partial exercise of this option by the underwriters financed VGAC up to the aforestated $509M. When the merger completes, VGAC shares and warrants will be converted to 23andMe shares and warrants, respectively. The warrants can be exercised for one class A share with a strike price of $11.50. The merger should be completed mid-2021.

23andMe shall have significant capital to accelerate its customer acquisition and drug discovery efforts. This includes advancing its wholly-owned checkpoint inhibitor (P006) toward first-in-human clinical trials. More details on this therapeutic program should be coming out soon. The recent out-licensing of its anti-IL-36 bsMab to Almirall proves that 23andMe is capable of generating valuable therapeutic assets from its biobank. With its unique position in the biotech industry, 23andMe may soon transition from being primarily known as a DTC genetic testing provider to that of a prominent drug developer.

Author information

Ergo Bio closely follows innovation in the biotechnology space and evaluates interesting drugs and deals. It is run by Vandon T Duong (LinkedIn), feel free to connect! I am a biotech enthusiast and a molecular engineer by training. I am also an avid consumer of news and research around precision medicine.

Ergo Bio pages

Disclaimer

This article serves informational purposes only and should be treated strictly as educational material, not as investment recommendation or legal advice. The information presented may be inaccurate or out-of-date. The contributing authors and editors disclaim liability for any errors or omissions. Any opinions expressed may change without notice. Ergo Bio LLC reserves all rights to the content generated through this resource hub (Ergo Bio Insights).