Noteworthy: Gilead Sciences at the center of biotechnology in 2020

First-in-class antiviral for COVID-19 and extensive M&A activity

The “Noteworthy” series of articles discuss remarkable biotechnologies, organizations, and events with significant influence on the advancement of mankind. These articles are dense with information and commentary, all of which contribute to the greater context of the biotechnology revolution.

Highlights and takeaways

Gilead’s antiviral franchise enables it to rapidly develop drugs against infectious diseases. In response to the unprecedented pandemic, remdesivir was quickly tested and proven to offer clinical benefit for patients with COVID-19. However, there are numerous challenges with the commercialization of antivirals.

To continue its growth, Gilead has to supplement its revenues by identifying alternative blockbuster drugs. The company has shifted its historical focus on antiviral drugs to anticancer drugs. This year, Gilead has spent over $27B to deepen its immuno-oncology pipeline, including the multi-billion dollar acquisitions of Forty Seven and Immunomedics.

From biotech startup to big pharma

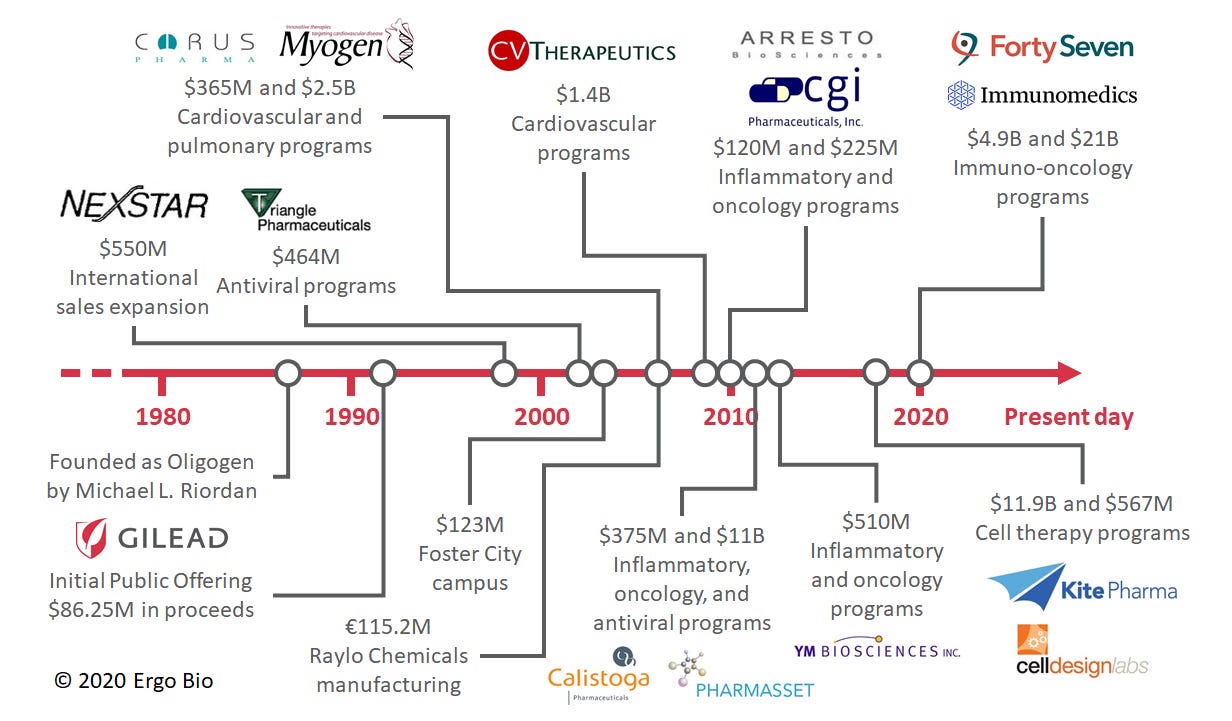

Founded in 1987, Gilead Sciences ($GILD) had a mission to develop an arsenal of antivirals using nucleotide chemistry (ref). Despite early challenges, the company achieved considerable success in developing efficacious antivirals and changed the standard of care for infectious diseases. With a prospering antiviral franchise, Gilead leveraged its strong cash position to make strategic acquisitions and continue to grow its therapeutic pipeline. This involved expansion into other disease areas, such as cardiovascular and pulmonary diseases. In recent years, Gilead has made numerous deals centered on inflammatory and oncology diseases.

This year, Gilead captured considerable attention due to its first-in-class drug for COVID-19 and its extensive business activity. Gilead pivoted its broad-spectrum antiviral, remdesivir (Veklury), as an experimental therapy for Ebola to an EUA treatment for COVID-19. Gilead also made multiple acquisitions and collaborative agreements to bolster their oncology efforts. In a way, Gilead is filling in the role left by Celgene as a major pharmaceutical acquirer, after they were acquired by Bistro Myers Squibb last year (ref). These two topics will be the focus of this article.

A robust antiviral franchise with drug pricing challenges

Among the pharmaceutical industry, Gilead is well known for its strong antiviral franchise: Cidofovir (Vistide) was developed for cytomegalovirus (CMV) infection and can slow the progression of CMV retinitis in patients with AIDS (ref). Emtricitabine/tenofovir (Truvada) was developed as a well-tolerated and highly efficacious pre-exposure prophylaxis (PrEP) against HIV infection (ref). Oseltamivir (Tamiflu) was developed as a medication to treat and prevent influenza (ref).

Source: Nobel Prize in Physiology or Medicine 2020

The company also developed an amazing cure, sofosbuvir (Sovaldi), for patients with hepatitis C. This drug enables most patients to have sustained virologic response, i.e. undetected hepatitis C virus in the blood (ref). The combination of sofosbuvir, peginterferon, and ribavirin allowed 90% of patients to experience sustained virologic response. Moveover, the combination of sofosbuvir and ribavirin was noninferior to the combination of peginterferon and ribavirin. Both treatment regimens allowed 67% of patients to experience sustained virologic response. The approval of sofosbuvir was notable because it shifted the standard of care away from interferon, which was less safe and tolerable. It also makes possible the eradication of an infectious disease without an effective vaccine (ref).

Gilead has marked notoriety for its pricing of sofosbuvir (ref). At the time, there were over three million patients with hepatitis C in the USA. A 12-week treatment course of sofosbuvir was priced at over $84k, instigating objections by patient advocates, insurance payers, and politicians. In response, the COO and president of Gilead, John Milligan, declared that “The value of a cure [is] underestimated in terms of the overall advantage to the healthcare system”. The annual revenue for its hepatitis C drugs, including sofosbuvir, peaked at nearly $20B in 2015 but has since rapidly fallen (ref). The efficacy of Gilead’s treatments had been so successful that it led to a massive decline in the number of patients afflicted by hepatitis C. Yet, the turmoil related to the pricing of sofosbuvir remains a big part of its history and has influenced the emergence of remdesivir for COVID-19.

Rapid clinical and commercial development of remdesivir

Remdesivir is a broad-spectrum antiviral that was originally investigated as a therapy for Ebola (ref). Preclinical studies demonstrated that remdesivir could potently suppress the Ebola virus within infected monkeys (ref). During the Ebola outbreak in the Democratic Republic of Congo, a randomized clinical trial was conducted to compare multiple monoclonal antibodies and remdesivir (ref). Remdesivir proved to be less effective than other monoclonal antibodies, such as Mab114 or REGN-EB3, at reducing mortality. While remdesivir was not approved for Ebola, the recent pandemic presented an opportunity for Gilead to rapidly repurpose the drug to target SARS-CoV-2, i.e. the coronavirus causing COVID-19 (ref). Preclinical studies established that remdesivir could robustly inhibit the replication of divergent coronaviruses, including SARS-CoV and MERS-CoV (ref). Furthermore, compared to other nucleotide analogs, remdesivir can potently inhibit coronaviruses with intact proofreading exoribonucleases (ref). This year, Gilead reported that remdesivir was capable of ameliorating respiratory symptoms and reducing viral replication in the lungs of monkeys infected with SARS-CoV-2 (ref). However, virus shedding from the upper respiratory tract was not mitigated despite reducing viral loads in the lower respiratory tract. Importantly, none of the sampled tissues expressed mutant RNA-dependent RNA polymerases known to confer resistance to remdesivir. As the first antiviral to demonstrate efficacy in COVID-19 animal models, remdesivir quickly proceeded as an investigational therapy for COVID-19 patients.

Source: Lamb 2020

Initially, remdesivir was available outside of clinical trials via compassionate use requests (ref). 68% of patients receiving remdesivir through compassionate use requests appeared to have improved clinical outcomes, specifically oxygen-support status (ref). Mortality by (a median of) 18 days was observed to be 13%. Unfortunately, patients receiving invasive ventilation were less likely to experience clinical improvement from remdesivir therapy compared to patients receiving noninvasive ventilation. While this assessment was on a compassionate-use cohort of patients and without placebo control, no new safety signals were observed.

In an adaptive, placebo-controlled trial sponsored by the NIAID, a 10-day treatment course was found to reduce the time to recovery from 15 days to 11 days (p < 0.001) (ref). Mortality by 14 days was reduced from 11.9% to 7.1%, but this was not statistically significant. However, it is important to note that the data and safety monitoring board had recommended to unblind the results even while the trial was ongoing. Subsequently, the investigators made the interim analysis publicly available and thus patients assigned to the placebo group could be treated with remdesivir. This preliminary assessment was based on 482 recoveries and 81 deaths, but the investigators will need to evaluate the remainder of the 1,063 enrolled patients. In an open-label trial sponsored by Gilead, a 5-day treatment course was found to offer similar benefit to that of a 10-day treatment course (ref). While this study was not placebo-controlled, the results suggest that the limited supply of remdesivir can be conserved with shorter treatment courses. In another open-label trial sponsored by Gilead, 5-day and 10-day treatment courses were compared to standard of care (ref). By day 11, the patients receiving 5-day treatment of remdesivir were 65% more likely to have improvement in clinical status compared to those treated with the standard of care (p = 0.02). Surprisingly, patients receiving 10-day treatment of remdesivir did not have a statistically significant difference from those treated with the standard of care. Collectively, the results of these three clinical trials allowed for the Emergency Use Authorization (EUA) of remdesivir as a treatment for COVID-19. At first, the EUA was for severely ill patients, but has since been broadened to encompass all hospitalized patients with COVID-19 (ref).

A placebo-controlled trial was also conducted in China, but the study was terminated early and it was not sufficiently powered due to limited patient enrollment (ref). Intriguingly, the WHO accidentally published a draft of the study results and later retracted it (ref). Gilead immediately issued a statement that “the post included inappropriate characterizations of the study” (ref). While remdesivir is not approved in China, it is conditionally approved in Taiwan, Canada, and the EU (ref). Japan has also approved remdesivir on the basis of the EUA in the USA (ref). Thus, remdesivir is the first approved therapy for COVID-19 in numerous countries. Gilead is still pursuing clinical trials with remdesivir, including its combination with other drugs like JAK inhibitor (baricitinib) or IL-6 receptor antagonist (tocilizumab). Gilead has also formulated an inhaled solution of remdesivir and is currently exploring its safety and tolerability in healthy volunteers.

The commercial development of remdesivir as a COVID-19 treatment was also hectic and rife with media spotlight. Perhaps this was due to both the unprecedented pandemic and Gilead’s controversial history with antiviral commercialization. Early on, Gilead sought and acquired orphan drug designation for remdesivir (ref). At the time, there were fewer than 200,000 confirmed cases of COVID-19 in the USA, so remdesivir technically qualified for the status. This would have granted Gilead numerous commercial benefits and financial incentives, including a period of market exclusivity, tax credits for running clinical trials, and a fee waiver for new drug application (NDA) or biologics license application (BLA). Patient advocates argued that remdesivir should not qualify for orphan drug designation because it would enable high drug pricing for a widely infectious disease. Soon after receiving orphan drug designation, Gilead requested to rescind this status and noted that regulatory submissions and reviews relating to remdesivir are still being expedited (ref). To be further transparent, the CEO and chairman of Gilead, Daniel O’Day, wrote an open letter discussing the pricing of remdesivir (ref). He commented that, based on the initial clinical results, remdesivir therapy offers an earlier discharge from the hospital and this would save approximately $12k per patient. Even so, remdesivir would be priced far below the value of this hospital saving. Each vial would cost $390 for government insurers and $520 for private insurers. Thus, a 5-day treatment course using 6 vials would cost between $2,340 and $3,120. Gilead has also donated their initial stockpile, 1.5M vials of remdesivir, to the government (ref). This donation lasted into July and the company has since begun collecting revenue for the drug. Recently, Gilead took back the distribution of remdesivir from the HHS and will be directly selling it to hospitals (ref).

Remdesivir could become a blockbuster drug, but its revenue will be lessened given the short duration of therapy, low price per vial, and challenges with global distribution. Furthermore, the slightly diminishing revenues of Gilead’s antiviral franchise (e.g. HIV/AIDS, hepatitis C) must be supplemented by alternative blockbuster drugs if the company is to continue its historical growth.

A shift from antiviral drugs to anticancer drugs

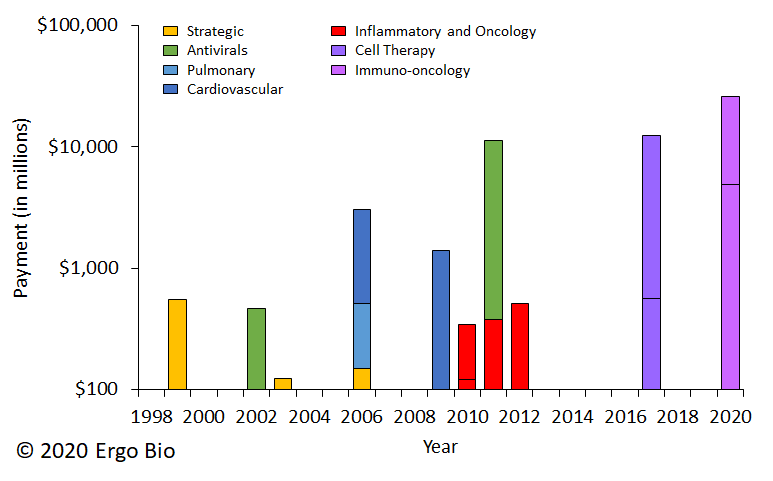

Gilead’s antiviral franchise is strong and routinely produces effective drugs, but faces challenges with pricing and revenue continuity. Thus, Gilead has been very prolific as an acquirer of startups in other therapeutic spaces, spending over $10B thrice on single acquisitions since inception. Before 2010, the company made multiple acquisitions of pulmonary and cardiovascular assets. Since then, there’s been a move towards acquiring inflammatory and oncology assets.

This year, Gilead made two massive, multi-billion dollar acquisitions. In March, Gilead announced that Forty Seven was to be acquired for $4.9B (ref). Gilead now owns magrolimab, an anti-CD47 antibody, which recently received Breakthrough Therapy Designation for myelodysplastic syndrome (ref). (related content: Trillium’s deal with Pfizer). In September, Gilead announced that Immunomedics was to be acquired for $21B (ref). Gilead now owns sacituzumab govitecan (Trodelvy), an anti-Trop-2 antibody conjugated with an active metabolite of irinotecan. This drug offered durable objective responses for patients with triple-negative breast cancer (ref). The deal came after Immunomedics reported over $20M net sales in the first two months of its commercial launch (ref).

Gilead also arranged numerous collaborative deals and licensing agreements. In May, Gilead established a decade-long partnership with Arcus Biosciences to co-develop and co-commercialize immuno-oncology programs (ref). Arcus’ portfolio includes AB154, an anti-TIGIT antibody, AB928, an adenosine receptor antagonist, and zimberelimab, an anti-PD-1 antibody. These molecules are under clinical investigation to determine if modulating the TIGIT or adenosine pathways can enhance the efficacy of PD-1 blockade (ref). Gilead shall provide an upfront payment of $175M, an equity investment of $200M, and milestone payments up to $1.6B. In June, Gilead paid $275M to acquire 49.9% equity interest in Pionyr Immunotherapeutics and the right to acquire the remainder for a $315M option exercise fee (ref). Pionyr is developing biologics to be used in combination with immune checkpoint inhibitors. In July, Gilead paid $300M to acquire 49.9% equity interest in Tizona Therapeutics and the right to acquire the remainder for up to $1.25B (ref). Tizona is developing TTX-080, an anti-HLA-G antibody, which is a potential immune checkpoint inhibitor. The decision for Gilead to exercise its option will likely come after phase 1b readout. In August, Gilead expanded its collaboration with Tango Therapeutics, which is using high-throughput CRISPR screening to identify novel targets of immune evasion (ref). Under this agreement, Gilead will provide an upfront payment of $125M, an equity investment of $20M, and up to $410M per program for rights to opt-in to up to 15 targets. In September, JTX-1811, an anti-CCR8 antibody, was exclusively licensed from Jounce Therapeutics for an upfront payment of $85M, an equity investment of $35M, and milestone payments up to $685M (ref). Preclinical data indicates that JTX-1811 preferentially depletes tumor-infiltrating T regulatory cells (ref).

Gilead has also made multiple agreements through its subsidiary Kite Pharma (acquired in 2017 for $11.9B), with most deal terms remaining undisclosed. In April, Kite licensed anti-BCMA antibodies from Teneobio to reformat it as a chimeric antigen receptor (CAR) (ref). A couple weeks after, Kite arranged a research collaboration with oNKo-innate to engineer natural killer (NK) cell therapies (ref). In September, Kite partnered with HiFiBio Therapeutics to identify novel targets and antibodies for acute myeloid leukemia (ref). Overall, Kite is making considerable progress with advancing its cell therapies, including the expansion of manufacturing facilities in Europe (ref).

Collectively, Gilead has spent over $27B to aggressively bolster its immuno-oncology pipeline this year. Despite the prominence given to its robust antiviral franchise, and especially its first-in-class antiviral for COVID-19, Gilead will likely be known for having a flourishing anticancer franchise in the coming years.

Author information

Ergo Bio closely follows innovation in the biotechnology space and evaluates interesting drugs and deals. It is run by Vandon T Duong (LinkedIn), feel free to connect! I am a biotech enthusiast and a molecular engineer by training. I am also an avid consumer of news and research around precision medicine.

Ergo Bio pages

Disclaimer

This article serves informational purposes only and should be treated strictly as educational material, not as investment recommendation or legal advice. The information presented may be inaccurate or out-of-date. The contributing authors and editors disclaim liability for any errors or omissions. Any opinions expressed may change without notice. Ergo Bio LLC reserves all rights to the content generated through this resource hub (Ergo Bio Insights).