Meta: Valuation and trading of competing biotech companies

Meta: Valuation and trading of competing biotech companies

Competition is often an indication of profitable opportunities

In a previous article, I briefly discussed various considerations when evaluating biotechnology companies, including key questions regarding the basic science, preclinical data, clinical trial design, financial positions, and management team. I also highlighted case studies on Aravive ($ARAV) and Replimune ($REPL) from the Mythos Biotechnology Fund, which I was a former partner of. In this article, I will draw attention to competing companies that are developing similar technologies, as well as the differences in valuation and stock trajectories. I will also discuss potential trading strategies centered on this, but these are not investment recommendations.

Biopharma is rife with competition and convergent technologies

Biotechnology holds considerable promise for creating new drugs and improving the standard of care. Often, great ideas are simultaneously pursued by multiple startups. The corollary is that consensus by competition is (somewhat) a validation of the underlying opportunity. If separate groups are willing to risk capital and exhaust resources on the same technologies or therapeutic targets, then there is likely a decent rationale. When it does work out, the successful companies may enjoy blockbuster sales despite competing for market share. Drug developers of PD-1/PD-L1 blockade are exemplary of this scenario. This is possible for other therapeutic spaces, including CRISPR gene editing, CD47 blockade, and bile acid modulation. I’ll briefly discuss each.

CRISPR gene editing startups

Source: Nobel Prize in Chemistry 2020 announcement

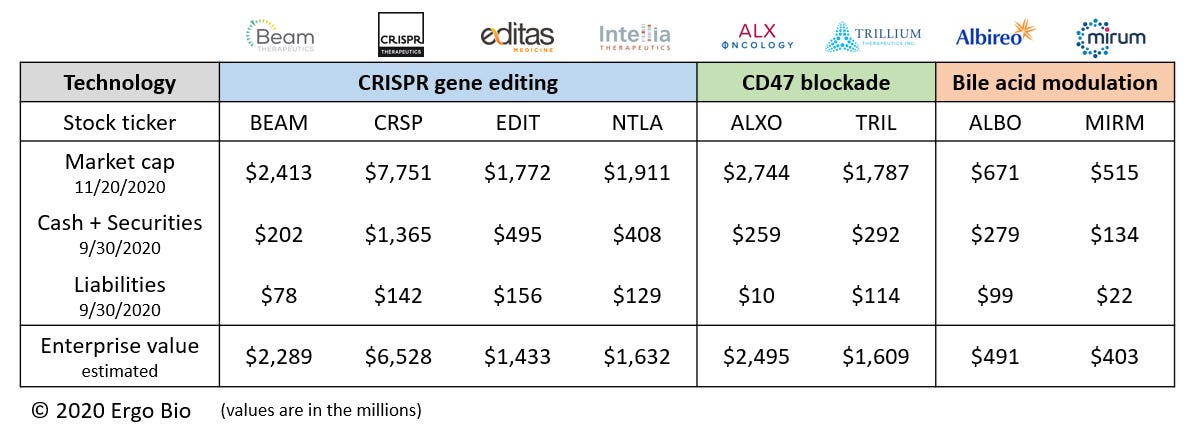

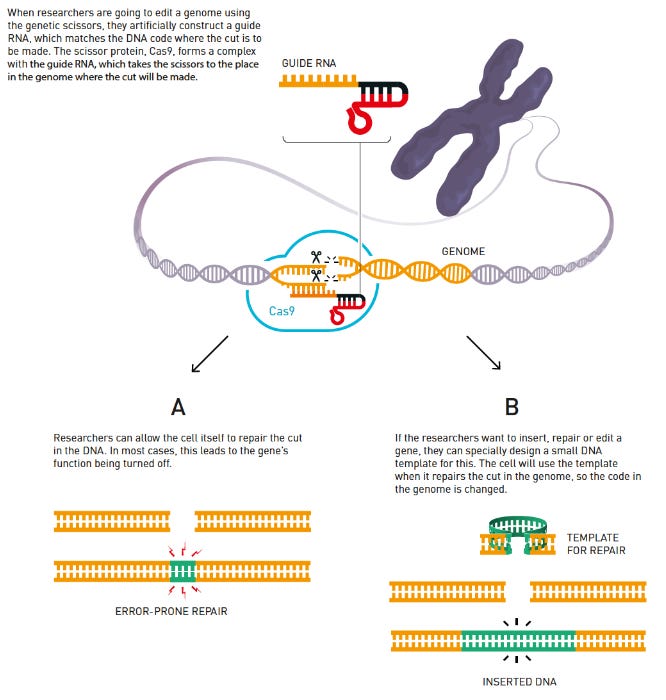

CRISPR gene editing was recently recognized by the Nobel Prize in Chemistry (ref). Specifically, Emmanuelle Charpentier and Jennifer A. Doudna shared the prize for the “development of a method for genome editing”. This induced considerable volatility in the trading of four major CRISPR gene editing startups: Beam Therapeutics ($BEAM), CRISPR Therapeutics ($CRSP), Editas Medicine ($EDIT), Intellia Therapeutics ($NTLA). Notably, CRISPR Therapeutics was co-founded by Charpentier and Intellia Therapeutics was co-founded by Doudna. These stocks experienced distinctly greater changes in share price and volume than Editas Medicines or Beam Therapeutics, which were co-founded by other CRISPR pioneers Feng Zhang and/or David Liu. Additionally, Beam Therapeutics differs from the other three in that its assets are at the preclinical-stage, so that could be a reason for its dampened performance.

Beyond volatility, there are significant differences in the valuation of the companies. CRISPR Therapeutics has a market capitalization that is multiple folds greater than the others. This could be due to its eponymous nature, loosely similar to the dotcom effect in elevating valuations during the turn of the century (ref). Another factor could be the differences in therapeutic pipelines and the market opportunity for the indications of focus. The clinical-stage assets for CRISPR Therapeutics include autologous hematopoietic stem cell (HSC) therapy for sickle cell disease and β thalassemia, and allogeneic cell therapies for blood cancers and solid tumors. Beam Therapeutics has similar assets as CRISPR Therapeutics but, as previously stated, these are at the preclinical-stage. The clinical-stage assets for Intellia Therapeutics include gene therapy for transthyretin amyloidosis and autologous HSC therapy for sickle cell disease. The clinical-stage asset for Editas Medicine is a gene therapy for Leber congenital amaurosis 10 (LCA10). There are also differences in the molecular engineering and delivery of the CRISPR systems by each company, which warrants careful and detailed discussion in a separate article.

CD47 blockade startups

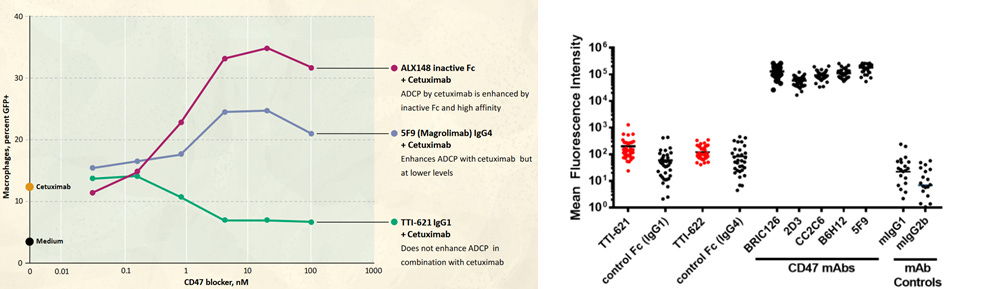

Source: Chao et al. 2012

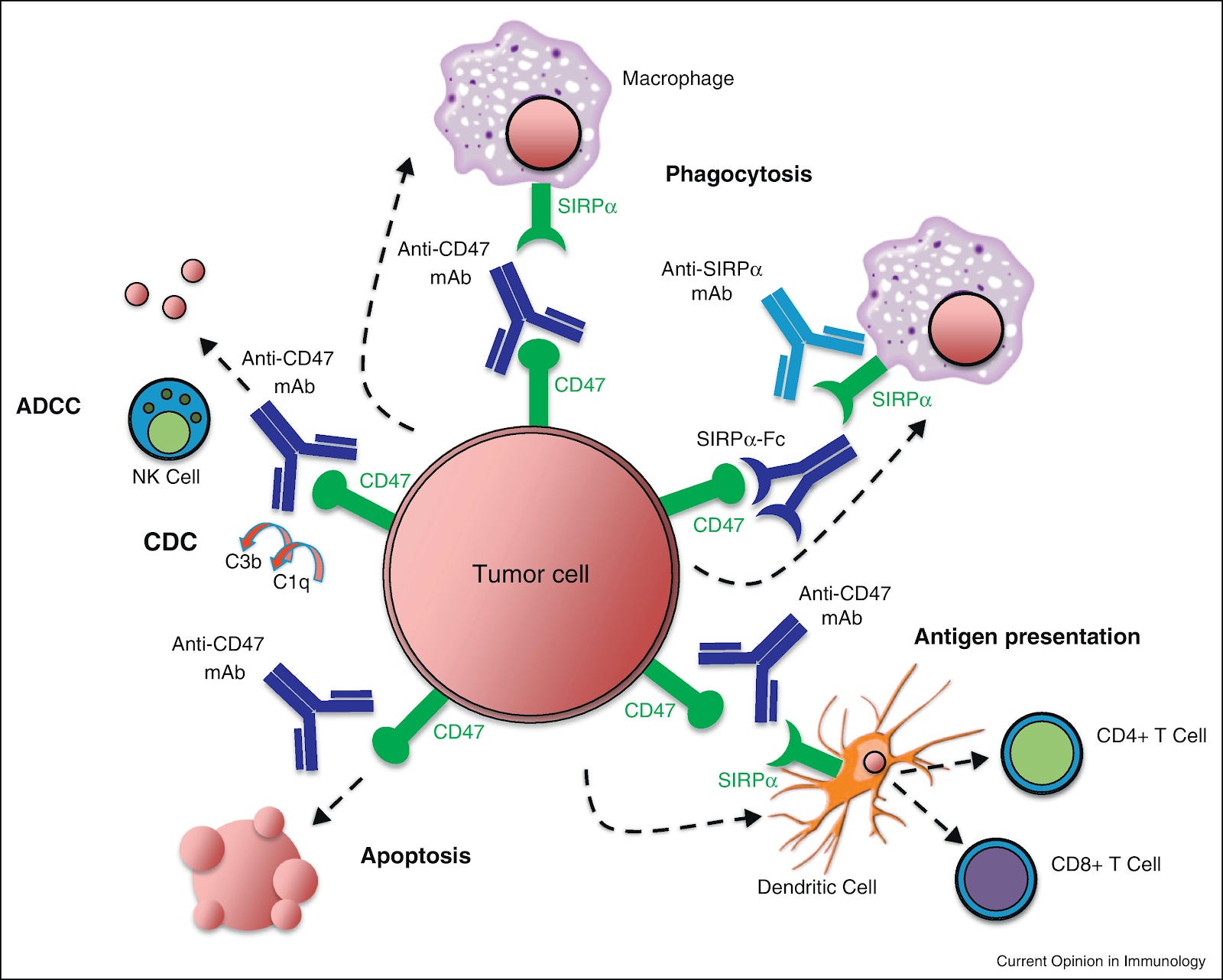

CD47 blockade is another exciting therapeutic modality for which multiple startups are testing in clinical trials, which was the topic of my first article. CD47 is a macrophage checkpoint which serves as a “don’t-eat-me” signal to discourage phagocytosis. The most clinically-advanced drug candidate is magrolimab from Forty Seven ($FTSV), which was recently acquired by Gilead Sciences ($GILD) for $4.9B earlier this year. Other startups developing CD47 blockade therapies are ALX Oncology ($ALXO) and Trillium Therapeutics ($TRIL). These have approximately $1B difference in valuations, which could be attributed to their distinct drug candidates, clinical trials progress, and partnerships. One week ago, ALX Oncology announced a collaboration with Zymeworks and that led to a 23% surge in share price (ref). Likewise, Trillium Therapeutics experienced an 11% jump in share price as third quarter results were released (ref). One could argue that the stock trajectories are related and influenced by the other. With the upcoming American Society of Hematology (ASH) meeting, the difference in market capitalization could widen, narrow, or even reverse.

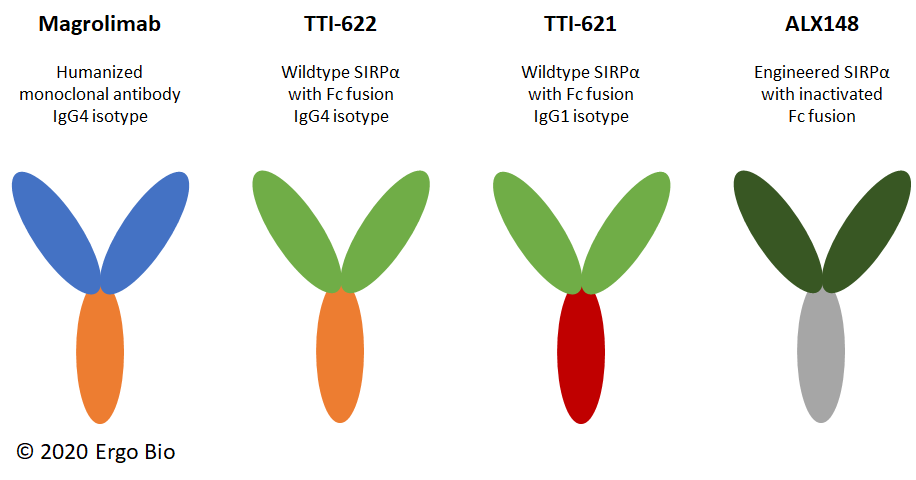

Differences in CD47 assets are highlighted here. Gilead now owns the rights to magrolimab, which received FDA Breakthrough Therapy designation for myelodysplastic syndrome in September (ref). It is a humanized monoclonal antibody that binds CD47 and blocks its signaling. Moreover, the IgG4 Fc domain mediates macrophage recruitment and activation. In comparison, Trillium Therapeutics is advancing two assets TTI-622 and TTI-621 which have the CD47 ligand SIRPα fused to Fc domains of differing isotypes. Compared with IgG4 isotype, IgG1 isotype could mediate stronger recruitment and activation of macrophages. The wildtype SIRPα has relatively lower affinity and thus less likely to kill red blood cells and cause thrombocytopenia. ALX Oncology has a single asset ALX148 which consists of engineered SIRPα and inactivated Fc domains, which enable tighter binding to CD47 without recruiting and activating macrophages. At present, Trillium Therapeutics is investigating its drugs as monotherapies for blood cancers, whereas AXL Oncology is exploring its drug in combination therapies (e.g. Keytruda, Herceptin, azacitidine, zanidatamab, rituximab) for blood cancers and solid tumors. Both companies have reported comparisons of their CD47 assets with others, which is of course favorably biased.

Source: ALX Oncology and Trillium Therapeutics corporate presentations

Bile acid modulation startups

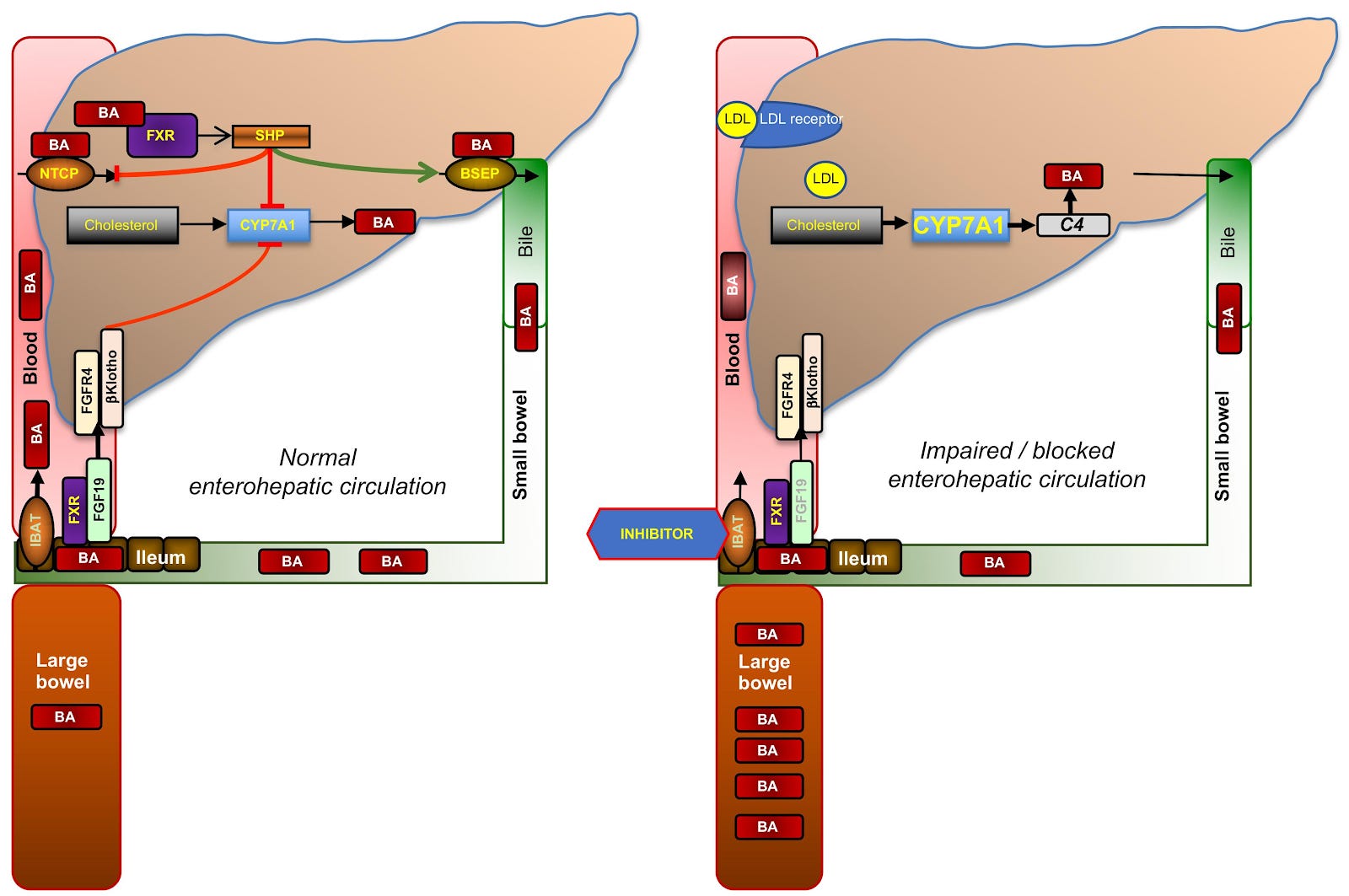

Inhibition of ileal bile acid transporter (IBAT) could be a treatment for liver diseases involving the accumulation of bile acid, such as chronic constipation, cholestatic pruritus, and non-alcoholic steatohepatitis (NASH) (ref). Bile acids are synthesized from cholesterol and serve to solubilize lipids by forming micelles. This helps with digestion and absorption of dietary fats and oils. The synthesized bile acids are excreted with bile into the small bowel, where it is then reabsorbed by the IBAT. This whole process is known as enterohepatic circulation. The impairment of IBAT leads to bile acid diarrhea and liver pathology.

Source: Al-Dury and Marschall 2018

There are two major bile acid modulation startups, Albireo Pharma ($ALBO) and Mirum Pharmaceuticals ($MIRM), that are investigating inhibitors of ileal bile acid transporter (IBAT) for Alagille syndrome (ALGS) and progressive familial intrahepatic cholestasis (PFIC). Specifically, pharmacologic blockade of IBAT could relieve patients of pruritus (itchy skin) and reduce the likelihood of requiring liver transplant (ref). Albireo is developing odevixibat and has partnered with EA Pharma to commercialize elobixibat, which is currently approved for treating chronic constipation in Japan. Mirum is developing maralixibat and volixibat. Given the similar assets and indications, these companies have relatively close valuations and their stock trajectories are highly correlated. However, Albireo overtook Mirum in September when they announced positive topline results for phase 3 study evaluating odevixibat for children with PFIC (ref). Alberio stock soared by 44.8% whereas Mirum stock dropped by 8.2%. It is reasonable to expect that both Albireo and Mirum will split market share for PFIC and ALGS, if the drugs get approved. There remains the possibility that only one drug gets approved and it is a winner-takes-all situation.

Potential trading strategies

Competing companies can serve as comparables for what valuations should be, as well as multiple opportunities for investing into a particular technology or indication. Therefore, the existence of competing biotech equities enable interesting trading strategies. I’ll describe some approaches at a high-level, but these are not investment recommendations!

One could construct a basket in which multiple securities under the same theme are owned. For example, if the investor had a strong conviction on the future of CRISPR gene editing, he/she could simultaneously go long on $BEAM, $CRSP, $EDIT, and $NTLA. Likewise, if the strong conviction was for CD47 blockade, the investor could go long on $ALXO and $TRIL. And of course, if the strong conviction was for bile acid modulation, the investor could go long on $ALBO and $MIRM. The basket could be weighted towards the favored underlying stock, and regardless catch upside momentum for the therapeutic modality as a whole.

One could also employ an arbitrage strategy with the similar securities. Traditionally, arbitrage refers to simultaneously buying and selling a given security that is priced differently on separate exchanges. It could also refer to trading on takeover events, where the valuation would greatly appreciate. Generally, the arbitrageur exploits market inefficiencies and trades on the hopes that prices will converge to their fair value. With biotech stocks, one could trade on the basis of an impending acquisition. The investor could also trade on new information, such as clinical trial results from a competitor.

In the event of a market-wide collapse, such as the one that occurred in March due to the COVID-19 pandemic, investors could also sell securities at a loss and buy other similar securities at a lowered price. This would not count as a wash sale, and therefore tax losses can still be recognized. However, this is allowed because the underlying securities are for independent companies and there remains considerable risk to make such a trade. For tightly correlated stocks, this could be a reasonable trading strategy.

Feel free to reach out if you want to discuss these in further depth.

Author information

Ergo Bio closely follows innovation in the biotechnology space and evaluates interesting drugs and deals. It is run by Vandon T Duong (LinkedIn), feel free to connect! I am a biotech enthusiast and a molecular engineer by training. I am also an avid consumer of news and research around precision medicine.

Ergo Bio pages

Disclaimer

This article serves informational purposes only and should be treated strictly as educational material, not as investment recommendation or legal advice. The information presented may be inaccurate or out-of-date. The contributing authors and editors disclaim liability for any errors or omissions. Any opinions expressed may change without notice. Ergo Bio LLC reserves all rights to the content generated through this resource hub (Ergo Bio Insights).